Two U.S.-regulated, dollar-denominated prediction markets began taking bets on the presidential race this week, with a month to go before Election Day.

Kalshi, which fought a long legal battle with the Commodity Futures Trading Commission to offer election contracts in the U.S., launched its presidential markets on Friday, following Wall Street powerhouse Interactive Brokers’ (IAB’s) ForecastEx, which did so the day before.

So far volumes are modest at both CFTC-supervised exchanges, with $344,101 worth of contracts traded on Kalshi and $346,000 on ForecastEx. By comparison, more than $1.2 billion has been staked on the race between Kamala Harris and Donald Trump at Polymarket, the crypto-powered prediction market platform, which, despite prohibiting U.S. users under a CFTC settlement, has reaped record volumes this year while Kalshi and IAB sat on the sidelines awaiting legal clarity.

“It will be hard for the two sites to catch up, but that is not entirely impossible,” said Koleman Strumpf, an economics professor at Wake Forest University in North Carolina. For one thing, “some traders may switch from Polymarket to the other sites,” he told CoinDesk. (Despite geofencing, American traders have reportedly been using VPNs to access Polymarket.)

Moreover, “more than half of all trades will happen between now and election day if history is any guide (and there is more volume for close races which this looks to be),” said Strumpf, who has studied the history of election markets.

However, Aaron Brogan, a managing attorney at Brogan Law, said that Polymarket has two advantages beyond being the first mover.

“Polymarket is theoretically accessible to people all over the world. In contrast, Kalshi’s products aren’t available to ‘foreign nationals‘ and certain other excluded groups,” he said. “Second, Polymarket doesn’t have explicit position limits, but Kalshi’s rules do. In this case, the limit is quite high, but it’s conceivable that this could be a limiting factor on total market size.”

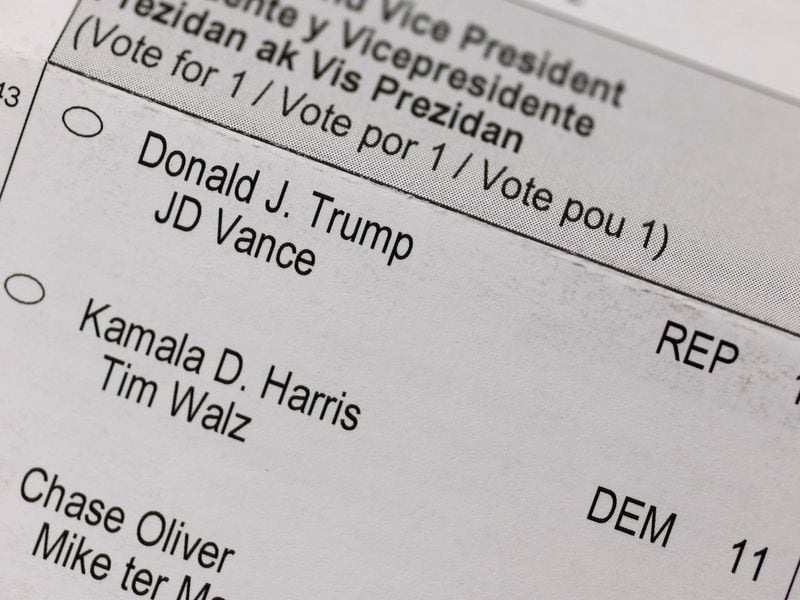

Early afternoon Friday in New York, prices of “yes” shares for Harris were trading at 51 cents, signaling traders give her a 51% chance of winning. Trump’s odds on Kalshi were at 50%.

Harris was also leading Trump on ForecastEx, but by a wider margin, 53-47. Meanwhile, on Polymarket, the two candidates were neck and neck, at 49% each.

Harry Crane, a statistics professor at Rutgers University in New Jersey, said these differences were not very meaningful. “We’re used to using polls in election forecasting, and with polls, there’s a well-understood margin of error, three percentage points usually, depending on sample size,” he said.

Similarly, in markets there is sometimes a “margin of inefficiency” where any profits to be made from arbitraging price differences are not worth the effort. “There’s no sufficient incentive for anyone to scoop up the penny that the difference might present.”

But prediction markets “don’t need to be identical to be useful for forecasting,” Crane said. Over time, observers can collect data on these markets, determine which ones had stronger predictive track records, and come up with a consensus forecast that might put more weight on one market than another, he said.

Kalshi sued the CFTC last year after the agency denied its application to list contracts on which party would control each house of Congress. The company won the case (which the CFTC is appealing) and listed the congressional contracts on Sept. 13.

They traded for only a few hours before the appeals court granted the CFTC an administrative stay freezing the contracts, which it lifted Wednesday. Emboldened, the company not only revived the congressional contracts but self-certified the presidential one. Self-certification is the process whereby CFTC-regulated entities list products without the agency’s prior approval. IAB, which started ForecastEx over the summer, quickly followed suit.

The CFTC, which is also considering a proposal to ban political event contracts at the exchanges on its watch, has asked the appeals court to expedite the case. Among other reasons, the agency said its proposed regulation “may be substantially impacted by this Court’s decision on the merits.”

But it’s apparently given up on stopping these contracts from trading before the election. Its proposed timetable would have briefs filed by Nov. 22 (more than two weeks after Americans cast their votes) and oral arguments heard on Dec. 2.

![[Action required] Your RSS.app Trial has Expired.](https://8v.com/info/wp-content/uploads/2026/01/rss-app-cfAqZL-350x250.png)